A dynamic response to digital challenges – HCL Technologies

The financial services industry has never had a better opportunity to embrace a customer-centric approach to doing business. Raising the bar for customer experience can create clear competitive advantages, and a responsive digital channel offering is essential. Here, insiders from the banking industry, the insurance sector and HCL Technologies' customer experience management principal discuss the challenges of remaining agile in the digital space.

There is a widely held belief that the financial services sector has been slow to respond to the changing demands of its customers, despite growing recognition that a customer-centric model will define the industry's future. As the industry continues to evolve in the digital age, it becomes imperative that financial services institutions of all kinds focus on delivering a consistent and high-quality customer experience.

Anne Boden, former chief operating officer at AIB, firmly believes that the banking sector cannot simply keep its head down and carry on as if nothing has changed.

"I think there is a certain amount of complacency that the existing model will stay as it is forever. Looking back over my career, which is over 30 years now, nothing much has changed. There is more that has been exactly the same than has really disrupted the industry. I think we are in a situation now - post-2008 financial crisis and with much more regulation in the financial services sector - where consumers want to see something different and are demanding better service. Something has to change," she remarks.

Interaction with customers through digital channels is increasingly important as mobile and online services become ever more popular. It is an arena where organisations can develop an agile and responsive service offering that keeps pace with what customers expect from providers of financial services.

Harvind Bhatti, principal - customer experience management at HCL Technologies, believes that a well-crafted and well-managed customer experience is a key differentiator for financial institutions, as well as a driver for overall performance.

"Institutions are increasingly realising that there is a strong link between a mature customer experience and better business outcomes," she says. "For example, globally, nearly 50% of customers close at least one banking product a year. For customers opening and closing accounts, the most important reason that influenced their decision was customer experience [more so than rates, fees and location].

"There are numerous studies that suggest that there is astrong correlation between advocacy [those customers who would recommend their primary institution to someone else] and trust. While overall financial stability is usually the top reason for complete trust, how customers are treated is the second reason, followed by other elements of experience such as complaints handling, communications and quality of advice. Therefore, treatment drives trust, which drives advocacy and, hence, there is a correlation with growth.

"The opportunity to provide better treatment and advocacy though customer experience has never been so big for the industry," continues Bhatti. "Relationships and service can be built and delivered ubiquitously and directly. Let's take technology services like Mobile Reach or the growing emergence of sensor-laden devices - both provide ways to improve the quality of engagement and service delivered, and in some cases, additionally support more cost-efficient methods of interaction."

The success of these and other tools is using them purposely in a well-crafted experience that supports genuine assistance in moments of need, or provides genuine additional value to a customer.

HCL is a global IT services company that specialises in software consulting services, enterprise transformation, remote infrastructure management, R&D and business process outsourcing. Financial services is one of its key verticals, and it is helping many organisations in the sector to rethink their approach to customer experience.

Financial institutions are appreciating more and more that customer experience is increasingly linked to their overall digital agenda, and that digital requires a permanent and fundamental change in the way business is done. It requires a total rethink of operational processes, professional skills and organisational culture to support the change.

"Customer experience requires becoming more engaged, intelligent and connected with a faster internal clock speed," Bhatti explains. "The challenge for brands is the organisational calibration of technology, culture, and ways of working and investment required.

For brands that were not born digital, navigating the most effective route to this capability is one of the biggest agenda items at the moment. Challenger brands, like the recently announced Atom Bank, are building entire propositions on customer experience and value. These brands are born digital, and have the inherent capability and mindset to mine the opportunity. Traditional brands have to transform and be 'reborn digital'.

"Everyone talks about customer needs, but their fundamental needs haven't changed - their expectations have. Our potential to better serve those needs is far greater, and customers know that from experiences within and outside our industry. The expectation to be consistently and seamlessly served across all channels and all product areas, for example, is a hygiene factor. For institutions, this is one of the hardest journeys they have faced. The journey to differentiation really only begins once you can top that."

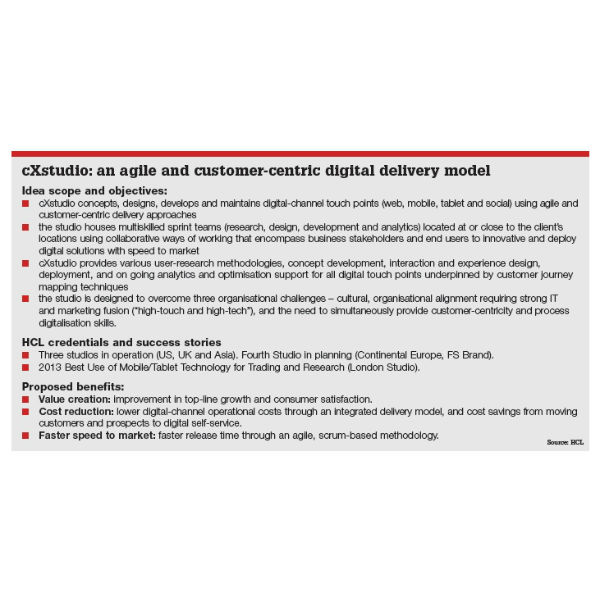

Having understood that the responsiveness and versatility of digital channels are key to the overall quality of customer experience provided by financial services institutions, HCL has developed cXstudio - customer experience studios - that help organisations deliver front-end customer experience.

HCL believes that digital channels need to be developed and optimised with the end user and overall channel ecosystem in mind. This is placing greater emphasis on organisations to have robust "learn, understand and act" processes with experience design capability that continuously defines user and business needs in the context of technical feasibility and agile processes that deliver digital channel solutions at the speed the market requires.

"These requirements are continuously increasing the cost of digital-channel delivery for organisations, and have proved difficult to implement due to the cultural change and organisational alignment required," adds Bhatti. "cXstudio is our customer experience studio, which we house on site or near our client organisations. The studios house multiskilled and multifunctional teams of business and IT experts who will co-create and co-develop channel projects using agile and customer-centric delivery approaches in collaboration with client stakeholders."

HCL has three studios currently in operation, with another additional studio planned in Europe. These studios bring together research, design, development, and analytics and maintenance capability to quickly deliver innovative digital solutions for change and run projects.

The ability these studios provide to continuously enhance concept development, customer experience and interaction, as well as optimise deployment times for digital solutions, helps clients to improve top-line growth, improve customer satisfaction and lower operational costs for digital channels. The core concept behind cXstudios is to fuse strong IT capability with marketing; support greater and faster alignment; and move faster and more robustly from business/consumer needs to delivering business/consumer value.

"Customer experience capabilities require a 'high-touch and high-tech' approach to front-end channel development and optimisation, and a speed of development that requires a more agile approach," explains Bhatti.

"Our cXstudios focus on delivering front-end digital-channel experience in a collaborative and agile delivery model. The studios are either co-located on clients' sites, or within walking distance of the client to support the iterative development of digital channel changes or optimisation. We begin with multiskilled teams at the start of the concept process, so there is an equal tension between marketing, business, creative, analytical, and technology skills in defining and eventually implementing the solution."

With accelerators such as cXstudios, the industry can start to take advantage of the opportunity that now presents itself to make a dramatic change in how it approaches customer experience. Boden believes that the industry has no time to lose if it is to take advantage of such a capability.

"We are at the start of things changing in the industry. The important thing is to start addressing what the customer wants rather than what we as institutions want to deliver. We have to stop looking at this from the point of view of an institution or of the financial services industry, let's think about what the customers actually want. They don't want us to keep on doing things the same way we always have, they want something different," she says.

Crossing the channels

The urgent need for financial services institutions to focus on digital channels as a powerful force in shaping customer experience has arisen because it is in this space that customers have attained greater control over their relationship with banks, insurers and pensions providers. They expect to be able to interact with these organisations from anywhere and at any time, just as they do with online retailers or with their network of contacts through social media. David Beattie, customer service director at life insurance, pensions and asset management company Aegon, sees this as a key driver of innovation in the pensions sector.

"Customers want us to be here outside of normal office hours, and that is perfectly valid. That is a big driver of Aegon's Retiready offering, which is a digital service for non-advised savers that enables them to assess their income needs and choose the right products, and Aegon Retirement Choices, which is a new online pension and saving platform that puts customers in control. Information is available 24/7 online, but we are also providing webchat support in the evenings and at weekends, as well as call-centre support. There are also dynamic FAQs that evolve in response to customers' needs," says Beattie.

"The biggest problem customers raise with us is that the changes in the pensions industry are not easy to understand. They want us to simplify it for them so they can secure their financial future. That is why the Retiready online service is designed entirely around customer feedback. It was built hand in hand with customers, and that in itself is a very good example of customer service. In the future, customers will want end-to-end digital services as long as they are simple to use. Our products should be as easy to use as Amazon, Google, Facebook or Twitter," he adds.

In the banking industry, the ability to interact with customers across many channels is at once an opportunity to form consistent and agile client relationships, and to glean the data on customers that is essential to providing that level of service. For Boden, the question is how to best use that data in a customer-centric model.

"When you look at the challenger banks coming from the retail space, for instance, you have to ask whether their brand can stretch far enough and whether customers will trust their data with those organisations. Banking is about far more than doing lots of analytics on your bank account and figuring out what to sell you next. I think using that data to sell you more, which is the retailer's model, could be very dangerous in the banking world. We have to take this balance very seriously. We have to use the client's data for the benefit of the client and not just take every opportunity to sell something off that data. Doing so could lead to the next big mis-selling scandal," she says.

"All people in the C-suite in big banks are constantly bombarded by people trying to sell us propositions to sell more. Consultants come in the door to ask how they can help us increase the number of products per customer. But isn't it flawed thinking to focus simply on trying to sell more? Shouldn't we be thinking about what we can do with the information and the technology we have in order to help our customers? That will help us to regain customers' trust. We all messed up in 2008, we lost the trust of our customers in many arenas, and we have a long way to go to regain that trust; we have to do that by acting responsibly," adds Boden.

Beattie agrees that using data is not just about selling more products, but rather about doing better by customers. He sees better information about customers as a starting point, not the sole determining factor in customer experience.

"Data analytics is important in this industry, and we have made steps in the last two years to better understand our customers, but the answers they need cannot just come from data. Human factors and emotional responses determine important financial decisions," he remarks.

HCL's cXstudio incorporates not only the analytics capability that can help financial institutions to create additional value from their customer data, but also the skills to put that data to use in the creation of better customer experience in the digital space and the contact centre. Bhatti believes that data should shape the human and digital interactions with customers.

"Data needs to play an even bigger role in call centres, for example. Not just to sell more products, but ultimately to create the 'wow' moment for consumers. Some consumers prefer to engage purely digitally, while others are redirected more increasingly to online self-service by brands that want to reduce costs. The call-centre experience therefore is increasingly becoming the litmus test of the quality of an institution's human interaction," she says.

"Data can play a role in simply ensuring that operatives are better informed about the customer. In most cases, the wider channel ecosystem is designed so that the call centre is the last channel used, and customers are calling with an issue. The need for a well-designed and seamless omnichannel infrastructure is key here - allowing operatives to be more proactive about the problem.

"For instance, for one of our leading global financial institutions, customer experience starts first with customer insight, having a deep understanding of who they are and what they're trying to accomplish. They are focused on designing an experience tailored for customers in their particular situation. They focus on big life events that their customers go through and make sure they build touch points across channels. For example, for customers who are coming out of active employment, they want to provide advice and solutions to meet the important needs that arise as they retire from work. They use all of the data and analytics they have to not only respond well when customers contact them in any channel, but also to get much more proactive in anticipating their needs and reaching out to them," she adds.

A matter of trust

Customers have more power than ever to influence the market, not only because it is simpler than ever to switch to a new service provider, but also because it is much easier to publicly express views that can impact an organisation's brand. In an industry that is still rebuilding its reputation after the financial crisis of 2008, brand integrity counts for a lot. Customers expect the same level of service from banks and pension providers as they do from big retailers, and the financial services sector has a lot of ground to make up.

When Boden speaks of the need to rebuild trust, it is a message that echoes throughout the financial services sector, and Beattie agrees that must be the prime focus of the industry when it considers customer experience and investment in its people and technology. Raising service levels across all channels of engagement shows that providers of financial services value customer relationships and understand what their clients need.

"There are a lot of challenges facing the financial services sector, but from the customer feedback we get, the big issue is trust because of the banking crisis in the UK. Customers need to trust us again. Trust can be destroyed in an instant, but it takes a long time to rebuild," he says.

"From the perspective of a pensions provider, we have to be open, honest and as transparent as possible. We have to explain the changes that are happening in the industry, that is certain, but above all, we need to provide good customer experience. Customers are engaging with us in new ways, and as their needs evolve, we need to evolve, too. A big part of that is digital services, and in that space, we need to provide additional, easy-to-use services online," he adds.

Any effort to improve customer experience has to start with a process of measuring current performance. This applies to physical as well as digital channels, and Beattie explains how monitoring performance in call centres provides the baseline for dynamic improvement.

"We record every single call from customers, employers and IFAs, so that we can review them and learn the important lessons for training. We also measure net promoter score by asking customers to rate us. If the NPS is positive, then we make that known to managers and staff, and if it is negative, then we know we have to motivate the teams. Responding quickly to metrics is very important," says Beattie.

"You definitely need the right balance between people and technology. You need the skills and experience people bring because if you don't it won't matter how good your technology is, as the knowledge won't be there. But you can't do everything by phone either, as it would be too expensive," he says.

Invest in change

When financial institutions have established a measure of their customer experience, they have the starting point from which to deploy models such as HCL's cXstudio, which provide a cost-effective element of a broad-based strategy of investment in people and systems. Today, technology defines the ability of financial services institutions to back up their front-end channel strategies.

"Technology is essential to bring all the elements of customer experience together, but many organisations have grown through acquisition or have inherited technology, so there is often a problem with latency in legacy systems. The cost and time implications to make the transformation for organisations are often huge," says Bhatti

Boden, who knows first-hand the challenges posed by legacy systems, sees the complexity of core banking technology as one of the biggest issues that banks must face, and it is something from which the industry cannot hide.

"Recently, one of the CEOs of the big banks in the UK announced its annual results and, as part of the presentation, he ran through the complexity of its IT infrastructure. He said the bank was reducing the number of projects from 500 to 100, and reducing the number of payments systems from 80 to ten. Banks are dealing with layer upon layer of legacy systems, so it is very difficult for them to reinvent themselves.

Some have chosen to set aside the old systems and migrate to a new set of systems, which has typically cost billions of dollars and taken about five years or more. It is very, very difficult to reinvent your infrastructure," says Boden.

"This renewal of systems is high-risk and very expensive, so if I were in their position, I would wonder if the bank could afford to put everything on hold for five or six years. It is a very difficult problem. There are two issues at play - cultural and technical. Banks have to learn to work across the organisations together on projects to get things done. It is about addressing the problem rather than looking at it as a big project. Small groups of people working across the organisation can get things live far quicker than you can in the traditional way. I am a big advocate of minimal viable products and agile technologies. That is the way to get through this quagmire of systems," she adds.

In the area of customer experience, Beattie feels that outsourcing can be a powerful tool in an organisation's armoury, though it will not resolve all of the technological and investment issues.

"We have outsourcing partners in the customer experience space, and our outsourcing is done on a tactical level. We use it where additional skills are needed, but we keep our core skills in house and we have a growing base in Edinburgh. We have a very strong skill base there that understands the pensions industry very well, so we have the capability to adapt our digital offering from there," he says.

"When it comes to balancing cost-efficiency with quality, you need to make sure you have the right blend of people and technology. You need to balance skills and experience on one hand with the ability to provide data-driven answers to fact-based questions in an online environment. It is when a customer has more than one question, or has a more complex issue to raise, that the contact centre becomes a better option, but then if you do too much by phone your costs go up. Customers may start their engagement with us by phone until they are more familiar with us, so you need to have that capability for personal interaction," he adds.

Whether customer interaction happens personally or digitally, the ability to be responsive and dynamic in the delivery of services defines the quality of customer experience.

"You must be proactive to understand what customers want. You have to look at recent data to predict the volume and type of requests. We listen to customers' views far more than the industry did ten years ago," says Beattie.

The analytics and development capability in HCL's cXstudios can be applied to human interactions as well as mobile or online services, as the company recognises that there is a broad palette of factors that impact customer experience.

"All work within the cXstudios is underpinned by insights throughout the process, and a strong customer-centric approach to channel interaction at a macro and micro level. As well as reading digital channels, we are using methods similar to those we use to look at social data, but applied them to the call centre. We turned the calls into text data and applied various algorithms not just to understand overall sentiment but more importantly, to understand specific issues. We reapply this insight into the formation of the wider omnichannel experiences we develop within the studios," remarks Bhatti.

"Transformation does not happen overnight, but the journey to becoming high-touch and high-tech can be quickened through accelerators like the cXstudio."

With the right support for technology development, marketing and customer experience financial services, brands can grasp what Bhatti rightly describes as a golden opportunity to differentiate and seek advantage. Solutions such as cXstudio that enhance customer experience are inevitably the models the industry can use to rebuild trust and gain the operational speed they require.

Harvind Bhatti is a principal and senior director at HCL Technologies. She has over 15 years’ experience in digital transformation from an IT and marketing perspective. Harvind has lived and worked in Germany. Previous to HCL, she was strategy director at SapientNitro and, earlier, VP marketing at Digitas.

Harvind Bhatti is a principal and senior director at HCL Technologies. She has over 15 years’ experience in digital transformation from an IT and marketing perspective. Harvind has lived and worked in Germany. Previous to HCL, she was strategy director at SapientNitro and, earlier, VP marketing at Digitas.

Anne Boden is the former chief operating officer of Allied Irish Banks (AIB) and an expert on the current banking sector. Born in Wales, Boden previously held senior roles with Royal Bank of Scotland, ABN Amro and insurer Aon.

Anne Boden is the former chief operating officer of Allied Irish Banks (AIB) and an expert on the current banking sector. Born in Wales, Boden previously held senior roles with Royal Bank of Scotland, ABN Amro and insurer Aon.

David Beattie is customer service director at life insurance, pensions and asset management company Aegon. He has 23 years’ experience in financial services (life, pensions and banking) as a director in operations; senior manager in change; senior manager in operations; delivery of business change; and IT programmes.

David Beattie is customer service director at life insurance, pensions and asset management company Aegon. He has 23 years’ experience in financial services (life, pensions and banking) as a director in operations; senior manager in change; senior manager in operations; delivery of business change; and IT programmes.